You’ve Got Options When It Comes to Home Financing

There are many mortgage options that can help make purchasing and maintaining a home more affordable.

Low down payment mortgage options, loans for manufactured homes, and a variety of renovation loans are all available to suit different buyers’ needs. It also helps to research these options before you find a mortgage professional who can help you choose the best one for your financial situation. Here are some options to explore:

Low down payment mortgage options

Balancing everyday expenses while also saving for a home purchase can be challenging. Fortunately, today’s buyers have mortgage options that allow for down payments well below 20% of the home’s purchase price. Some may even be able to buy a home with as little as 3% down.

Homeownership education requirement

In order to qualify for a HomeReady, HFA Preferred, or 97% LTV loan, you may be required to complete homeownership education.

Fannie Mae HomeView® is a comprehensive online course that is offered free of charge and can be used to satisfy the requirement.

Affordable mortgage options are available for manufactured homes

Manufactured homes can be a more affordable option compared to site-built homes. There are a variety of modern, attractive models built to high standards with many of today’s sought-after amenities. Manufactured homes can come with attached garages, upgraded kitchens and bathrooms, energy-efficient appliances, and architectural features that blend seamlessly into a variety of neighborhoods. The main difference is they’re built indoors in efficient state-of-the-art facilities, and then delivered and installed on your chosen home site.

For borrowers looking to purchase a manufactured home that is built to meet construction, architectural design, and energy-efficiency standards more consistent with site-built single-family homes, MH Advantage® could be the right mortgage loan option.

Is an MH Advantage loan right for you?

- This loan allows for 30-year fixed-rate financing.

- The down payment can be as low as 3%.

- You have the flexibility to fund your down payment through multiple sources, including gifts and grants.

- There is a potential for lower interest rates compared with other manufactured home financing.

- There is an opportunity for cancelable mortgage insurance once you reach 20% equity in your home.

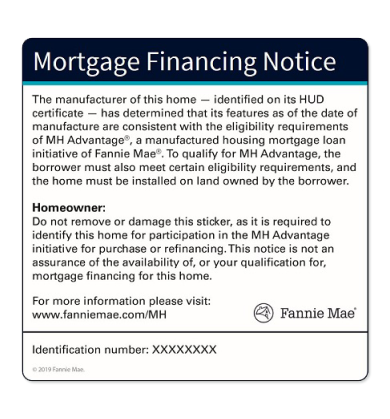

Why does the MH Advantage sticker matter to homeowners?

The MH Advantage sticker, like the one shown here, identifies homes that meet the standards for an MH Advantage mortgage. The presence of this sticker means that you, and any future buyer of the home, will be eligible for MH Advantage financing, including the benefits mentioned above.

MH Advantage stickers are usually applied near the HUD Data Plate (a government-required sticker) in a discreet location, such as in the utility closet or in a cabinet under the kitchen sink.

If the sticker is removed or damaged, it may impact the ability of the property to qualify for MH Advantage financing in the future, such as in cases of refinancing or resale. If your MH Advantage sticker is removed or damaged, contact the manufacturer of the home to see if a replacement sticker is available.

Mortgage options for homes needing renovations or energy updates

If the home you love is just in need of an upgrade, there are affordable financing options for renovations and energy updates. And to make it easy, you often get to work with the same lenders you’re already working with for your mortgage.

Even more affordable options for homebuyers

There are many additional affordable paths to buying property and building equity for your future.

Many types of affordable mortgage loans are available to homebuyers with options to suit different income levels and financial situations. Learn about as many as you can so that you can make an informed decision about your future as a homeowner.

More to explore

Down Payment Assistance Search Tool

Loans, grants, and gifts are three ways to supplement your savings for a down payment. Use this search tool to find and apply for financial assistance.

Get to Know the Types of Mortgage Loans

Choose the best home loan for your needs by learning about common loan types such as fixed-rate, adjustable-rate, FHA, USDA, and VA loans.

Homebuying and Homeownership Costs

From your down payment and closing costs to unexpected bills for home repairs, here are the expenses to prepare for as a new homeowner.

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count